A smarter way to model charitable giving inside long‑term tax planning

Charitable giving has always played a meaningful role in retirement planning, but until now, most planning tools treated it as an afterthought—or ignored it entirely. With a recent update to the Roth IRA Conversion Optimizer, that changes in a big way.

Your Optimizer now includes support for both Qualified Charitable Distributions (QCDs) and Donor‑Advised Funds (DAFs), allowing you to model charitable strategies with the same precision as Roth conversions, RMDs, and tax‑efficient withdrawal sequencing.

This upgrade matters because charitable tools aren’t just philanthropic—they’re powerful tax levers. And now they’re integrated directly into your long‑term projections.

🎯 Why Charitable Tools Matter in Retirement Tax Planning

Qualified Charitable Distributions (QCDs)

QCDs allow individuals age 70½ or older to donate up to $100,000 per year directly from an IRA to a qualified charity. The benefits are uniquely strong:

- The distribution does not count as taxable income

- It reduces the taxable portion of the current year’s RMD, which can, in turn, help avoid IRMAA surcharges, NIIT, and bracket creep

- It reduces future RMDs by lowering the IRA balance

- It’s often more tax‑efficient than donating cash

In many cases, QCDs are the single most powerful charitable tool available to retirees.

Donor‑Advised Funds (DAFs)

Before age 70½, QCDs aren’t allowed—so DAFs become a go‑to strategy. Unlike a QCD, you cannot fund a DAF directly from an IRA. To use retirement funds for a DAF, a taxable IRA withdrawal must be made first, and those proceeds are then contributed to the DAF.

A DAF allows you to:

- Make a deductible charitable contribution that offsets income—especially beneficial in high‑income years

- Invest the funds for tax‑free growth

- Distribute grants to charities over time

- Smooth out charitable giving across retirement—and future generations

It transforms a standard line item in your financial plan into an active, hands-on tool for family philanthropy.

🧠 How the Optimizer Now Handles QCDs & DAFs

The new feature adds a single user‑editable column—the DAF/QCD column—that automatically adapts based on age:

- Before age 70½: entries are treated as DAF contributions from an IRA distribution

- Included in taxable income

- IRA balance automatically reduced

- Charitable deductions, if applicable, can be entered by the user in the income column (as a negative number)

- After age 70½: entries are treated as QCDs

- Excluded from taxable income for the current year

- Current year’s RMD automatically reduced

- IRA balance automatically reduced

This dual‑purpose design keeps the interface clean while giving you full control over charitable strategy modeling.

For DAF contributions not requiring an IRA withdrawal, enter the amount in the One-time expense column so it doesn’t impact the IRA balance.

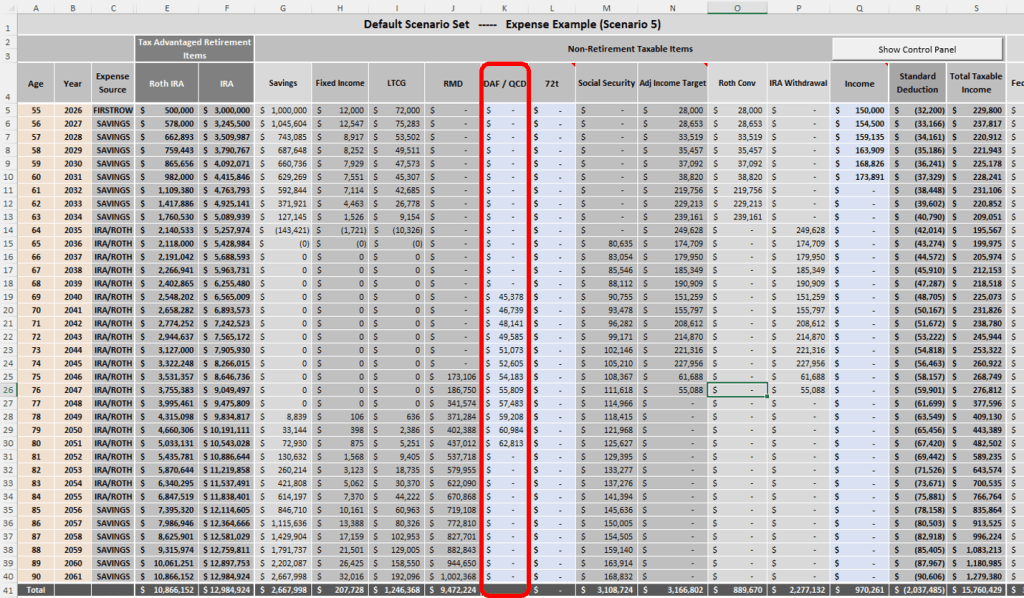

📊 What This Looks Like in the Optimizer

In the attached scenario image, you can see how the new DAF/QCD column flows through the entire model:

- IRA balances drop in the years with charitable distributions

- RMDs shrink in later years

- Taxable income adjusts correctly depending on whether the entry is a DAF or QCD

- Federal tax liability reflects the charitable strategy

- Net worth projections incorporate the reduced IRA balance

The result is a fully integrated charitable giving engine inside your long‑term tax plan.

🚀 Why This Matters for Real‑World Planning

Charitable strategies aren’t just “nice to have”—they’re often the difference between:

- Staying under IRMAA thresholds

- Avoiding unnecessary capital gains taxes

- Reducing lifetime RMDs

- Smoothing taxable income across retirement

- Improving Roth conversion efficiency

- Developing a multi-generational philanthropy framework (DAFs)

By modeling DAFs and QCDs directly in the Optimizer, you can now see the true lifetime impact of charitable giving on taxes, cash flow, and net worth.

🧩 A More Complete Retirement Tax Engine

This update brings the Roth IRA Conversion Optimizer closer to what real‑world planning requires: a unified model where charitable giving, RMDs, Roth conversions, Social Security, and taxable income all interact dynamically.